Corporate Credit Risk and Investor Sentiment

The Excess Bond Premium

During my time at the Fed, I used to work with a model quantifying sentiment in the credit market. Like financial asset prices generally, this decomposed credit spread measure is a forward looking metric and contains information on the real economy. As such, this measure is a significant factor in predicting the probability of being in a recession over the next 12 months. Given these attributes and outputs of the model, this statistic was closely monitored by policymakers and market participants and is regularly updated by the Fed. In this post, I briefly go over the construction of this metric (EBP), and visualize the recent movements and the implications.

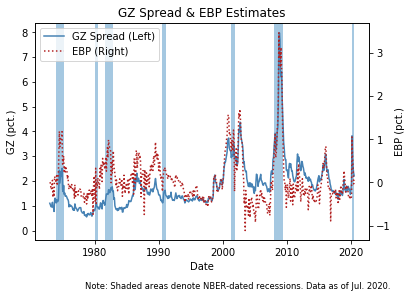

Both the GZ credit spread and the EBP have increased significantly prior to or during most of the cyclical downturns since the start of the sample. Additionally, since March this year, the EBP climbed to levels last seen in the early summer of 2008, just a few months before the nadir of the financial crisis; however, this pronounced deterioration in credit market sentiment has receded, but remains slightly elevated relative to pre-pandemic levels.

In terms of what this Python code does, I pull data updated in a FEDS Note and access recession dates from a FRED API. Additionally, I create some pretty figures which include two y-axes, and include shading during recession periods.

Introduction

Gilchrist and Zakrajšek (2012) (GZ), introduce a corporate bond credit spread by using data from secondary market prices of senior unsecured bonds. Yield spreads for each underlying corporate security are derived from a synthetic risk-free security that mimics the cash flows of that bond, bypassing any duration mismatch problems. This gives the monthly GZ spread, an average across firms:

where denotes the number of bonds in month

and

is the spread of firm

’s bond

in the same month.

Individual credit spreads are estimated using linear regression to remove a measure of expected default risk (Merton’s distance to default). By assuming the log of the credit spread on bond k to be linearly related to a firm-specific indicator of default (DFT) and a set of bond characteristics () like the duration, amount outstanding, the coupon rate, age, and if the bond is callable, we have:

Assuming normally distributed pricing errors (), the predicted level of the spread for bond

of firm

at time

is

where and

are the point estimates of the parameters and

being the estimated conditional variance of the pricing errors. This is the part of the credit spread that can be attributed to a firm’s specific expected default risk.

Like above, the aggregate credit spread portion directly attributable to expected default risk is given by the average of predicted spreads in month is:

Lastly, the rich and highly informative, residual component of the credit spread called EBP is the differenced measures of credit spreads:

This procedure decomposes the calculated GZ credit spread into two parts: , a component that captures default risk of individual firms; and

, a residual component that can be thought of as capturing investor attitudes toward corporate credit risk or credit market sentiment.

The references included argue that the EBP attempts to capture the variation in the average price of bearing U.S. corporate credit risk above and beyond the compensation that investors in the corporate bond market require for expected defaults. As documented in the GZ paper, the EBP is significantly more informative–in both economic and statistical terms–about future economic activity than a component of the GZ credit spread that can be directly attributed to expected defaults. Additionally, the EBP measures offers additional information that is not captured by the term spread, another spread used to predict future economic activity.

Below, I offer some code that pulls the most recent vintage of the EBP measure supplied by the Fed.

Load the EBP data and NBER recession dates from FRED API

import csv

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

from fredapi import Fred

fred = Fred(api_key='3d98a695a7a09b42b521a09547990f22') # own API key. Very easy to get your own

# load in EBP data

ebp_link = "https://www.federalreserve.gov/econresdata/notes/feds-notes/2016/files/ebp_csv.csv"

ebp_data = pd.read_csv(ebp_link, index_col='date',parse_dates=True )

# load Fred data

recession_dates = pd.DataFrame(fred.get_series('USREC'))

recession_dates=recession_dates.rename(columns={recession_dates.columns[0]: "recession_dummy"})

# inner join on the date index

ebp_data = ebp_data.join(recession_dates, how='inner')

# convert from float to integer

ebp_data["recession_dummy"] = ebp_data["recession_dummy"].astype(int)

# generate footnote for figures

last_date=ebp_data.index[-1]

Note = "Note: Shaded areas denote NBER-dated recessions. Data as of %s." %(last_date.strftime('%b. %Y'))

ebp_data.info()

ebp_data.tail()

ebp_data.describe()

Note: Shaded areas denote NBER-dated recessions. Data as of Jul. 2020.

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 571 entries, 1973-01-01 to 2020-07-01

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 gz_spread 571 non-null float64

1 ebp 571 non-null float64

2 est_prob 571 non-null float64

3 recession_dummy 571 non-null int64

dtypes: float64(3), int64(1)

memory usage: 22.3 KB

| gz_spread | ebp | est_prob | recession_dummy | |

|---|---|---|---|---|

| count | 571.000000 | 571.000000 | 571.000000 | 571.000000 |

| mean | 1.804665 | 0.060766 | 0.249950 | 0.134851 |

| std | 0.945770 | 0.555843 | 0.193779 | 0.341864 |

| min | 0.548800 | -1.113400 | 0.014413 | 0.000000 |

| 25% | 1.222300 | -0.292400 | 0.119239 | 0.000000 |

| 50% | 1.608300 | -0.069700 | 0.182572 | 0.000000 |

| 75% | 2.106300 | 0.261400 | 0.308726 | 0.000000 |

| max | 7.984000 | 3.467300 | 0.999701 | 1.000000 |

fig = plt.figure()

ax = fig.add_subplot(111)

lns1 = ax.plot('gz_spread', data=ebp_data, color="steelblue", label = 'GZ Spread (Left)')

ax2 = ax.twinx()

lns2 = ax2.plot('ebp',data=ebp_data, color="firebrick", linestyle='dotted', label = 'EBP (Right)')

# better legend

lns = lns1+lns2

labs = [l.get_label() for l in lns]

ax.legend(lns, labs, loc=0)

ax.fill_between(ebp_data.index, 0,1, where=ebp_data['recession_dummy'], alpha=0.4, transform=ax.get_xaxis_transform())

# format legend

ax.set_xlabel("Date")

ax.set_ylabel(r"GZ (pct.)")

ax2.set_ylabel(r"EBP (pct.)")

plt.title('GZ Spread & EBP Estimates')

plt.figtext(.95, -0.05, Note, ha='right', va='bottom',

fontsize='small')

plt.show()

Clearly, the two measures are highly correlated and have both experienced a large increase in recent months.

Clearly, the two measures are highly correlated and have both experienced a large increase in recent months.

Predicting Recessions

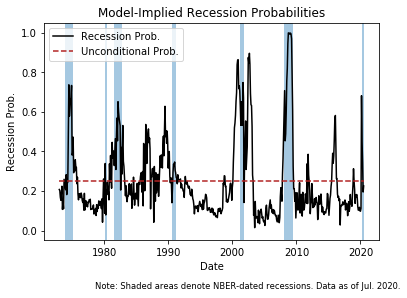

To isolate the role of credit market sentiment in U.S. business cycle fluctuations, the Fed kindly reports the in-sample fitted probability of a recession over the subsequent 12 months using the specification:

Which is reflected in Table 3 of this FEDS Note. As shown by the solid line, this probability has moved up significantly since the start of the year, peaking around 0.70 in March, coinciding with an increase in financial market volatility, and a deterioration in investor sentiment in the United States and abroad due to the Coronavirus. These concerns that triggered deterioration of investor sentiment apparently abated over the spring and summer, and the corresponding EBP-implied odds of the economy falling into a recession over the subsequent 12 months moved down to roughly 20%.

# plot recession probability

fig, ax1 = plt.subplots()

ebp_data['uncon_mean'] = ebp_data['est_prob'].mean()

ax1.plot('est_prob', data=ebp_data, color='black', label="Recession Prob.")

ax1.plot('uncon_mean', data=ebp_data, color='firebrick', linestyle='dashed', label="Unconditional Prob.")

ax1.fill_between(ebp_data.index, 0,1, where=ebp_data['recession_dummy'], alpha=0.4, transform=ax1.get_xaxis_transform())

ax1.set_xlabel('Date')

ax1.set_ylabel('Recession Prob.', color='black')

ax1.legend()

plt.title('Model-Implied Recession Probabilities')

plt.figtext(.95, -0.05, Note, ha='right', va='bottom',

fontsize='small')

plt.show()

plt.close('all')

# Subset data for a window since pandemic

sub_data=ebp_data.loc['2020']

# plot

fig = plt.figure()

ax = fig.add_subplot(111)

lns1 = ax.plot('ebp', data=sub_data, color="firebrick", linestyle='dotted', label = 'EBP')

ax2 = ax.twinx()

lns2=ax2.plot('est_prob', data=sub_data, color='black', linewidth=1, label="Recession Prob. (Right)")

# Better legend

lns = lns1+lns2

labs = [l.get_label() for l in lns]

ax.legend(lns, labs, loc=0)

# format plot

ax.set_xlabel("Date")

ax.set_ylabel(r"EBP (pct.)")

ax2.set_ylabel(r"Recession Prob.")

plt.title('2020 View: EBP & Recessions')

plt.show()

Conclusion

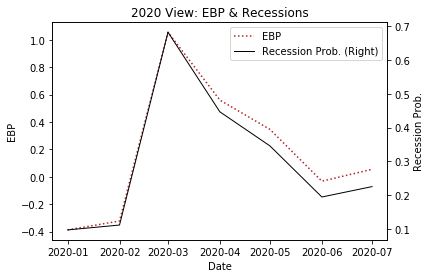

Retrospectively, it is not surprising to see an EBP spike in March, it is interesting that the measures have steadily tapered off over the spring and summer (with a slight uptick in July), but levels remain elevated relative to pre-pandemic levels suggesting that the economy has not fully recovered.

The model is specific to credit market sentiment, which can be heavily influenced by large fiscal stimulus targeted to keep firms solvent. With policy remaining at an impasse and surrounded by uncertainty, this would be an interesting set of figures to monitor over the next months to gain some insight as to depth of the recession.

References

Favara, Giovanni, Simon Gilchrist, Kurt F. Lewis, and Egon Zakrajsek (2016). “Recession Risk and the Excess Bond Premium,” FEDS Notes. Washington: Board of Governors of the Federal Reserve System, April 8, 2016, http://dx.doi.org/10.17016/2380-7172.1739.

Favara, Giovanni, Simon Gilchrist, Kurt F. Lewis, Egon Zakrajšek (2016). “Updating the Recession Risk and the Excess Bond Premium,” FEDS Notes. Washington: Board of Governors of the Federal Reserve System, October 6, 2016, https://doi.org/10.17016/2380-7172.1836.

Gilchrist, Simon, and Egon Zakrajšek. 2012. “Credit Spreads and Business Cycle Fluctuations.” American Economic Review, 102 (4): 1692-1720.